We would like to express our sincere gratitude to our shareholders, investors, and other stakeholders for their continued deep understanding and support of our company.

Based on the 14th Medium-Term Management Plan (FY2024–2026, hereafter "the 14th MTP") announced in May 2024, we are working to enhance our corporate value over the medium to long term. In the domestic environment and energy business, which is the pillar of the Group’s growth, the 14th MTP is positioned to realize the growth story toward the realization of the long-term Vision 2030 by giving priority to the investment of management resources, especially in orders for municipal solid waste treatment plants (renewal projects and primary equipment improvement projects) and the establishment of a revenue model that fully utilizes recurring revenue. Against the backdrop of a solid market environment, we recognize that our efforts are making steady progress, with record-high consolidated orders received of 246.3 billion yen in FY2024 (ended March 2025), and in May 2025, we revised upward the target figures of the 14th MTP. In addition, the 14th MTP establishes quantitative policies, including cash allocation, to achieve both business growth and shareholder returns that meet market expectations while maintaining a strong financial base.

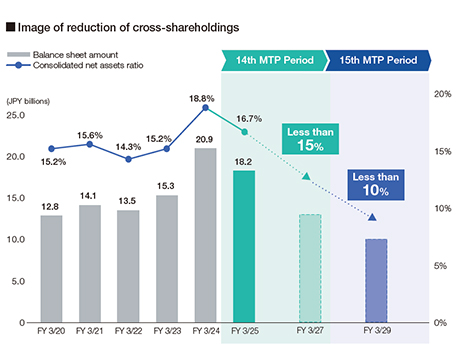

Since the announcement of this medium-term management plan, we have continued to actively engage in dialogue with our shareholders and investors with the aim of further enhancing our corporate value. Based on the feedback we received through the dialogue, the Board of Directors has held ongoing discussions, and in November 2024, we formulated a new policy to reduce cross-shareholdings. Specifically, the Group plans to reduce its cross-shareholdings to less than 15% of consolidated net assets by the end of FY2026, the final fiscal year in this medium-term management plan (a reduction of approximately 7 billion yen), and to further reduce them to less than 10% by the end of FY2028 (a further reduction of approximately 3 billion yen).

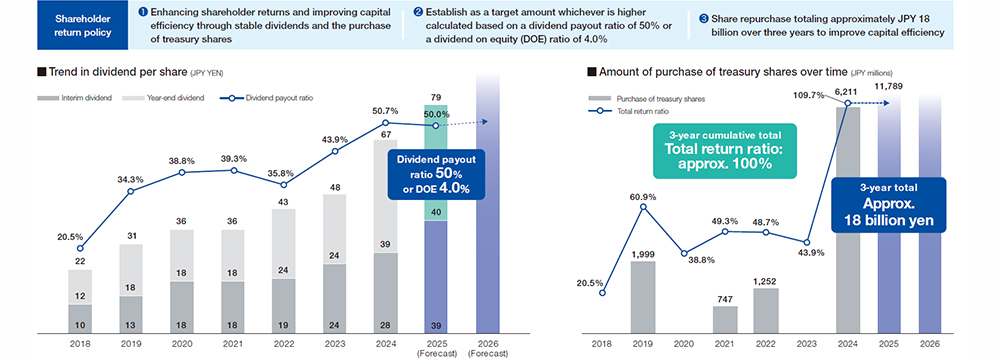

The Company’s policy is to use the cash generated by improving the efficiency of its balance sheet, mainly by reducing cross-shareholdings, for shareholder returns in the form of dividends and the purchase of treasury shares. In particular, the revised plan calls for the purchase of treasury shares totaling 18 billion yen over the three-year period, compared to the 12 billion yen envisaged when the plan was formulated. Including the dividend payout ratio of 50%, the total return ratio for the three-year period of the 14th MTP is expected to be approximately 100%, and we intend to realize further profit returns to our shareholders.

While strengthening shareholder returns, we will also focus on flexible growth investments to sustainably increase corporate value. Here, we introduce one of the growth investment projects resolved for FY2024, which is the acquisition of shares in IHI Packaged Boiler Co., Ltd. In its Vision 2030, the Group has positioned the Package Boiler Business, which consists of the general-purpose boiler business and other businesses, as an “ongoing business” that aims to steadily expand its earnings. Nippon Thermoener Co., Ltd., our consolidated subsidiary, has been handling this business since 2005, from product development and manufacturing to sales and service. Through this share acquisition, IHI Packaged Boiler became our consolidated subsidiary on April 1, 2025, and we expect that the product lineup and technological capabilities of both companies, which have a large share of the domestic market, will be combined to expand our competitiveness by establishing a supply system for products and services with higher added value. In addition, with the aim of further realizing synergies from the integration, the merger of Nippon Thermoener and IHI Packaged Boiler is scheduled to take effect on April 1, 2026. In the domestic environment and energy business, we will continue to proactively gather information on M&A opportunities that contribute to strengthening our capabilities, including human resources, as well as expanding our business domains, and to make flexible investment decisions.

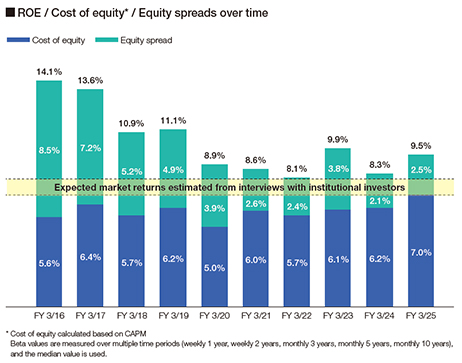

Our analysis assumes that the cost of shareholders’ equity, as estimated by the CAPM (Capital Asset Pricing Model), has increased to about 7%, taking into account the impact of rising long-term interest rates. In addition, based on interviews with institutional investors, the expected market return is estimated to be around 7% to 8%, which we believe does not deviate significantly from the cost of capital estimated by the CAPM. While the cost of capital is rising, ROE is also improving (9.5% in FY2024) through increased profits and improved capital efficiency, thus ensuring a certain equity spread (ROE minus cost of equity). At the same time, we recognize that our shareholders and investors expect an even higher level of equity spread. In order to meet the expectations of stakeholders, we have set our ROE target at 11.5% or higher for FY2026, the final year of this medium-term management plan, and at 12% or higher for FY2030, the final year of Vision 2030. We will achieve this goal by continuing our efforts to both increase profitability and improve balance sheet efficiency while maintaining a strong financial base. nt decisions as we strive to create sustainable corporate value.

Last but not least, the support of our shareholders, investors, and all other stakeholders is essential for us to realize our vision. We will continue to actively engage in highly transparent dialogue with you and utilize your opinions in our manageme